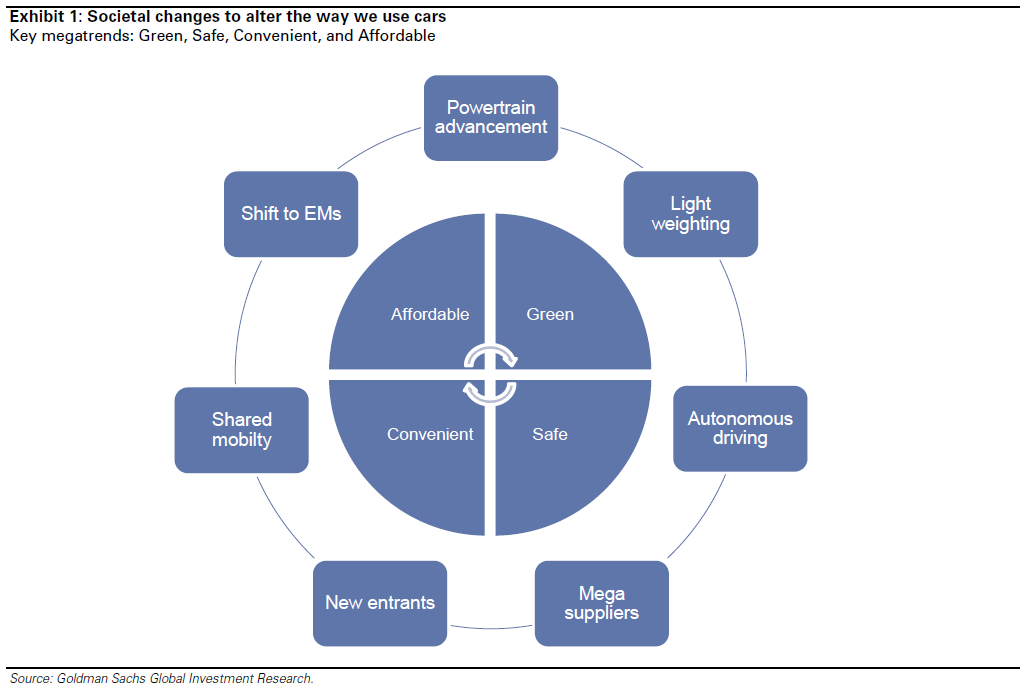

A Goldman Sachs research team recently came out with what they believe are seven automotive trends that will impact the industry in the next decade. How likely are they to become reality? Let’s look at the key points:

A Goldman Sachs research team recently came out with what they believe are seven automotive trends that will impact the industry in the next decade. How likely are they to become reality? Let’s look at the key points:

1. Endless powertrain advancement: Electrified vehicles will become 25% of global car sales by 2025

2. Autos on a severe diet: A 50kg drop in vehicle weight cuts CO2 emission volume by 1g per km. New materials to reduce car weights

3. Autonomous driving on horizon: Google wants to realize Level 4 automation by 2017. Autonomous driving could change society

4. Power shift to mega suppliers: Meeting CO2 regulations will cost automakers US$2,500 per vehicle. We expect the presence of mega suppliers to expand

5. New entrants afoot: The appearance of autonomous driving and EV is removing auto business entry barriers

6. Connected cars and shared mobility: Networked cars changing business models for industries from insurers to rental fleets

7. Shift to emerging markets: Motorisation in emerging markets continues unabated. By 2025, we expect China to have 35 mil vehicles and India 7.4 mil vehicles

It’s never easy to look into the crystal ball because the pace of technology change now renders strategic competitive advantages to a very short half-life. Where before new tech gave you a head start of years, today that’s been reduced to months, if not days. While the points raised by Goldman are interesting to say the least, a closer look does raise a few questions.

Here’s Countersteer’s take on their predictions:

1. Endless Powertrain Advancement

The move towards alternative power-trains may not be as quick as predicted. Regulation is a bigger push factor than economic realities as fossil fuel remains the most economical source of energy for cars (sad but true). Factor in the strides still being made by the internal combustion engine and the argument for alternative energy is less persuasive. Expect to be filling up dino-fuel for a while more.

Depending how one defines “electrified” (there is after all a huge difference in terms of electrification between that of a Nissan Serena Hybrid and a Leaf), but if it includes hybrids (HEV) and plug-ins hybrids (PHEV), then 25% might well be attainable by 2025 as many upcoming new models will offer a plug-in variant (e.g. the new Volvo XC90) though they are still primarily powered by internal combustion engines complemented by a relatively modest battery pack offering less than 50km worth of electric range.

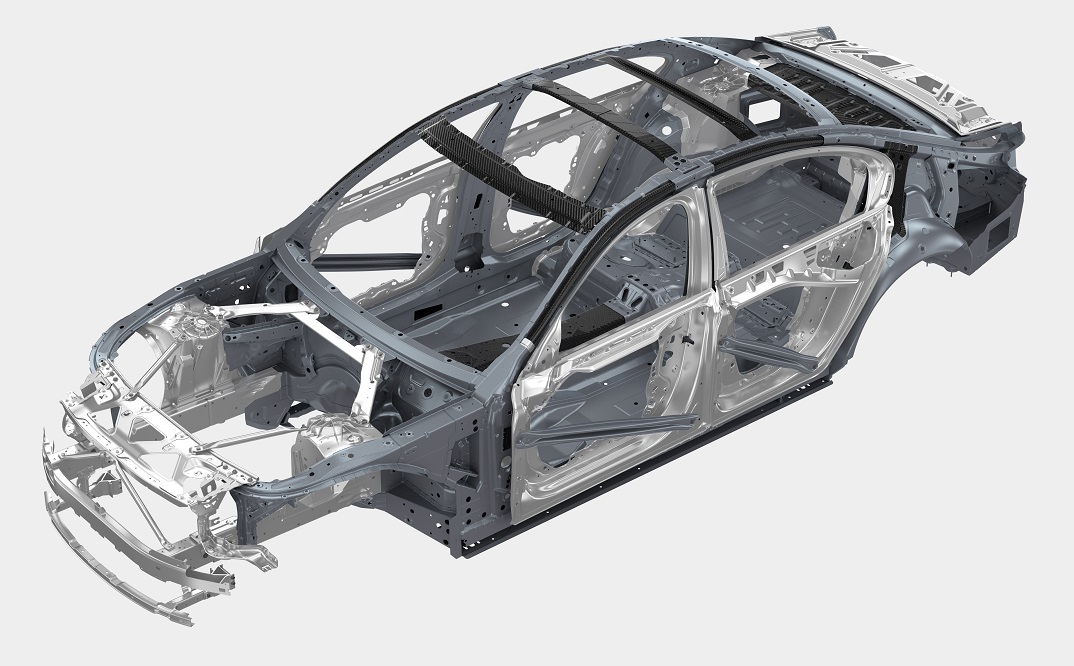

2. Autos on severe diet

No argument here. Lean is mean and the race to lop of the extra kilos will continue (the most recent exhibit being the new 7-Series with its carbon-fibre reinforced monocoque)

3. Autonomous driving on horizon

This is more wishful thinking than fact. Level 4 autonomous driving requires so much disruptive change from a regulatory and infrastructure perspective that it’s unlikely to happen in the next decade, maybe even the next few decades. We can’t see governments coming together and agreeing to embrace autonomous driving. It will be extraordinarily costly (for governments and car makers) and the legislative process will be arduous to say the least.

What we will find though is more “intelligent” Level 3 aids like lane change guidance, auto-braking, self-parking to move up the chain a little and play a more active role. Perhaps we might see a Level 3.5 of sorts.

4. Power shift to mega suppliers

This has been happening over the last decade and is not likely to change. The downside of mega suppliers is of course global ramifications when something goes wrong – think Takata. Additionally, car makers loathe to become overly dependent on a handful of suppliers.

5. New entrants afoot

This one is a little dodgy. While Tesla is shifting a respectable number of premium-priced Model S in its home country, it is less successful in other key markets (such as China). The industry has been building fuel powered cars and will continue to hone internal combustion technology as long as fuel is readily available and affordable. Google and Apple are showing keen interest but currently, it is Tesla against the rest of the world, and new entrants have never been able to significantly impact this industry. However, the China factor might well come into play.

6. Connected cars and shared mobility

6. Connected cars and shared mobility

Maybe in highly dense metropolitan areas where space and cost become astronomically prohibitive but by and large, this is still a “no”. Convenience trumps cost all the time. You need to go some where? Get into your car. No fuss, no hassle and that isn’t going to change soon. Though our best wishes to Cosmo – Malaysia’s first EV car sharing programme – we hope they succeed because electric vehicles deserve a chance.

7. Shift to emerging markets

Don’t need to be a rocket scientist to agree with this one!